Are you keeping track of your inventory? An inventory management system is what you need.

As a business, you know how important your inventory is to the day-to-day. It is equally important to always keep track of it as accurately as possible. This is where an inventory management system comes in handy.

Regardless of being brick-and-mortar or e-commerce, inventory is often the lifeline of a business. This means that as a business owner or manager you need to always know what your inventory situation is at any given point. Are you running low on a product? Or have you overstocked to the point where it’s costing you in storage? Neither scenario is ideal for any business.

Having a reliable inventory management system will help you maintain a balance of items at hand and reduce the possibility of error.

A quick refresher

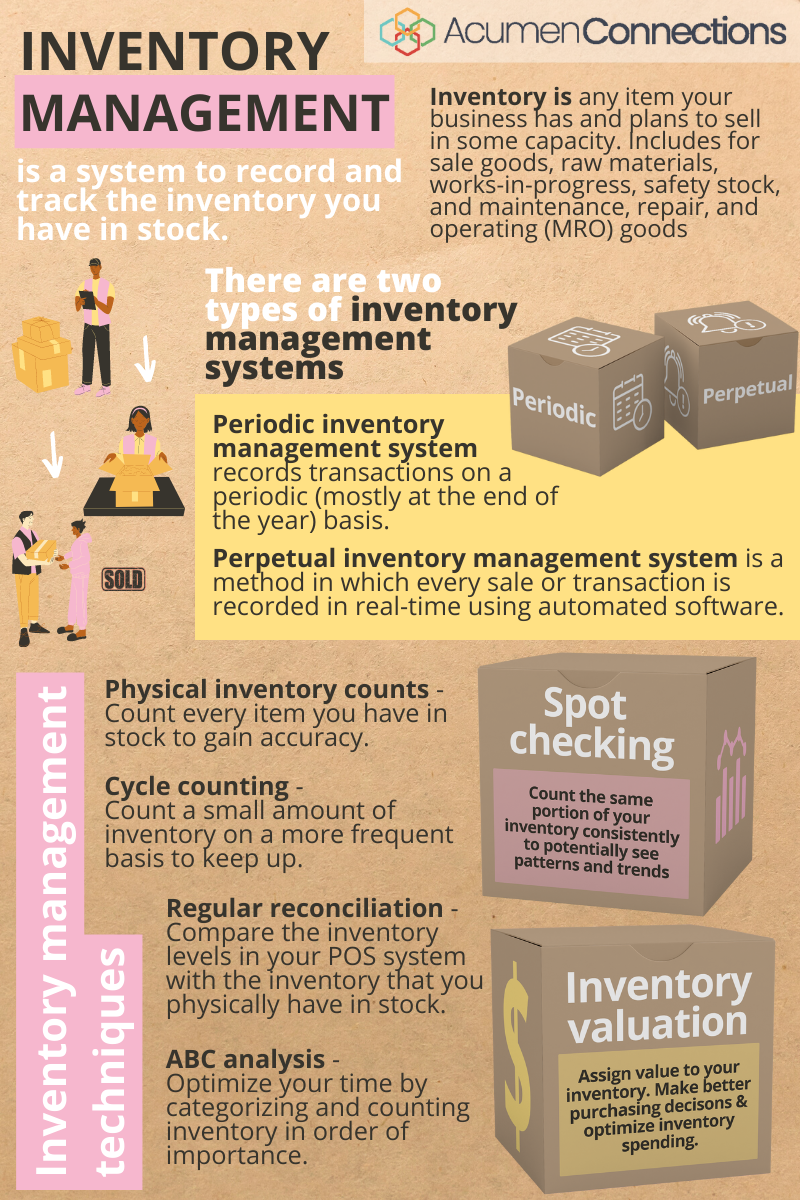

Inventory is any item your business has and plans to sell in some capacity. Examples could include retail items or software you plan to sell as-is to businesses or consumers. It could also include any raw materials you have to buy to make your products.

Some common types of inventory include the following:

- For sale goods: Products that have been made and are ready to sell to customers.

At a bakery, fresh bread would be considered for sale goods. - Raw materials: Items that will be turned into goods for sale.

At a bakery, flour would be considered raw materials. - Work-in-progress: Items that have already started the manufacturing process but aren’t ready to be sold.

At a bakery, cake batter would be considered a work in progress. - Safety stock: Additional items you keep on hand to help cover sales in the case of an unexpected supplier shortage or sudden surge in demand.

At a bakery, they might store a couple extra bags of flour or sugar in a separate room – just in case. - Maintenance, repair, and operating (MRO) goods: Items used for the care of the day-to-day operation and maintenance of machinery.

At a bakery, dish soap would be an MRO good.

What is inventory management?

Definition: Inventory management is the system by which a business keeps track of what items and quantities they have in stock. This allows them to coordinate ordering new shipments, along with managing storage and carrying costs. The end goal is to minimize losses and maximize profitability.

Benefits of inventory management system

There are several reasons inventory management systems are important for a business. Their prime benefits are:

- Giving an accurate report on inventory status

- Being able to order new shipments in time

- Tracking and managing seasonal products

- Helping prevent loss or theft

- Keeping up with demand fluctuations

- Observing trends to improve sales techniques

- Preventing overstocking and understocking

- Avoiding unnecessary carrying and storage costs

- Improving efficiency and ROI (return on investment)

- Accomplishing all the above in a time-efficient manner

How to use inventory management to help with purchasing

Purchasing inventory isn’t as simple as just placing an order for a product. There are several factors to consider when buying inventory, including cost. That’s why using an inventory system is recommended when purchasing inventory as it is less prone to human error and is convenient to use. The inventory purchasing process involves three simple steps. They are:

Planning

Good planning is often at the core of several successful ventures in business and in life.

First of all, not all businesses can afford to bulk buy or store an exorbitant amount of a product. Secondly, they need to estimate how fast or slow one batch of a product sells. They would also need to factor in the time required for a shipment to arrive and be prepared (listed, counted, stocked on shelves, etc.) for sale. Then you can set a budget for the purchase.

Using an inventory management system can help predict demand and sales trends to offer a realistic glimpse into your profit margins.

Buying

Now that you’re done with planning and have a budget, you can get to the buying stage. Many POS (Point of Sale) system have built-in orders. This helps you keep track of all your orders and once your shipment arrives, you can scan the inventory to receive into your system.

Please take care to ensure that you don’t mess up the ranking of categories you had set previously but do add new categories if necessary.

Managing

Once the inventory is received into your system, it needs to be managed. Set up schedules for counts and checks along with monitoring performance. Make adjustments to reorder points if deemed necessary based on sales or other supply chain factors.

If you are unable to move inventory at the rate necessary, you might need to consider making changes to your buying or selling strategy. This will help you avoid tying up dollars in stale inventory and storage.

Inventory management system types

There is more than one inventory management system that businesses can adopt.

The periodic inventory management system records transactions on a periodic (mostly at the end of the year) basis. Alternatively, the perpetual inventory management system records transactions as soon as they happen.

Need a visual? This graphic helps highlight the two major types of inventory management systems:

Perpetual inventory system vs. periodic inventory system

The prime difference between the perpetual inventory management system and periodic inventory management system is when transactions are recorded. The former keeps records in real-time while the latter does it at the end of the year.

Both systems were adopted by businesses in the past. Today, larger businesses are frequently opting towards using the perpetual inventory management system for the day-to-day. Small businesses with less inventory are opting for periodic inventory management.

What is perpetual inventory management? A closer look

The reason behind the increase in popularity of the perpetual inventory management system? Thanks to technology, we now have access to automated software, which makes the process convenient and practically error-free.

This system allows you to be aware of your inventory levels at all times. The key factor here is automation that almost nullifies the possibility of human error.

You can access stock levels, which are updated as soon as a change occurs. This is true for both physical stores and online businesses. Be it an in-person checkout or an online checkout, perpetual inventory management updates your inventory record as soon as the transaction goes through. It prevents you from ordering too much of a product as well as from the risk of depleting reserves before you can place an order.

Although the whole process is automated, we would recommend inspecting your inventory every now and then to rule out damage or loss of any kind.

A perpetual inventory system example would be scanners in grocery stores. These scanners scan the barcodes of products and record all transactions as they happen. The system stores details such as how many units are available and how many have been sold.

Pros:

- Speed and efficiency

- Less human error

- Automated (with minimal manual checks)

- Can help with small business accounting

Cons:

- Expensive upfront

- Requires manual audits regardless due to loss

What is periodic inventory management? A closer look

In comparison, the periodic inventory system requires physically counting units of products in your inventory. The periodic system is known to be time-consuming and prone to error, especially for large warehouses.

Smaller businesses may not face that same level of concern – it depends on the size of their business and the products they sell.

To make the periodic process easier, some businesses break up the work throughout the year by counting stock quarterly instead. This helps them save time at the very end of the year.

In a periodic system, all inventory purchases and store sales are based on the cost of goods. It could be the cost of new goods, or the cost of goods sold (COGS).

Whereas perpetual inventory management often looks at the number of inventory items, periodic inventory management looks at the COGS.

The technology for perpetual inventory management may be more expensive upfront. However, over time, periodic inventory management becomes more costly. Consider the cost of time and manpower year after year.

Pros:

- More affordable upfront

- Ideal for businesses with commonly low levels of inventory

- Can better identify loss due to theft or damaged goods

- Allows you to calculate COGS easily and focus on your margin

Cons:

- Requires more time, energy, and manpower

- Always an estimation – not recorded in real-time

Periodic may be great to start with, but as you grow, perpetual inventory management may be the way to go.

What are the best inventory management software solutions?

We have compiled a list of the top inventory management software in 2022. Check out:

Tips for effective inventory management

Effective inventory management can create increased profit margins, among other benefits. Follow these pointers for effective inventory management in a business:

- Categorize inventory by priority

- Track product information

- Periodically audit your inventory

- Determine supplier reliability

- Maintain a consistent process

- Embrace technology

Inventory management techniques

The inventory system types (perpetual and periodic) are largely based on the frequency that inventory is counted. Inventory management techniques are actions and ways of thinking to carry out the counting and understanding of inventory. Let’s explore a few inventory management techniques employed by businesses:

1. Inventory valuation method

This refers to what or how much your inventory is costing you. Knowing this is important as it helps you make better purchasing decisions. It’s a key part of business and a key part of inventory management.

Total cost of inventory = Purchase Cost + Ordering Cost + Holding Cost

Buying too much or too little can cause problems. Buying too frequently or not frequently enough can also have similar impacts.

Inventory valuation can help you determine how to optimize inventory spend. Let’s explore a few inventory costing methods. These methods will allow you to assign value to your inventory:

A. The retail method

When using this method, you get an approximate value of your ending inventory. It’s easy to calculate but doesn’t consider changing costs, and it’s not the most accurate. This method works best if your store has a lot of various products, with very similar markups.

How to find the approximate cost of your inventory? Use this formula:

Cost-to-retail ratio = (price per unit / retail price per unit) x 100

Formulas:

- COGS = Revenue x cost-to-retail ratio

- Alternative COGS = Revenue x [(price per unit / retail price per unit) x 100]

- Closing inventory = (Cost of goods available ÷ Retail amount of goods available) x Estimated ending inventory at retail

B. The specific identification method

In this method, a specific cost is assigned individually to every single item in a store. This can be tedious for large businesses with huge inventory, but it can help small businesses get a more accurate picture of their profits and losses. It’s especially useful for small businesses with high-value or rare items, where precision is necessary. Think of an antique or jewelry shop.

The items are best tracked via the use of an RFID tag, serial number, or receipt date.

Formulas:

- COGS = Units sold x Price per unit

- Closing inventory = (Purchase quantity – Units sold) x Price per unit

C. The first in, first out (FIFO) method

Even if you buy the same items month over month, sometimes prices can change. These next two inventory management technique methods both consider that the price you pay for inventory changes over time.

When using FIFO, it is assumed that any item sold was from the oldest batch you had in stock. It’s easy to understand this method. However, it may be easier said than done. Organization is key for this method.

The reasoning behind FIFO is that as inflation happens, the costs of goods go up. Since older items are sold first, the ending inventory is thought to be worth greater value. FIFO works best for businesses that sell duplicate items with a short shelf-life.

Formulas:

- COGS = Units sold x Price per unit from oldest applicable inventory purchase

- Closing inventory = Total value of inventory – (units sold x price per unit from oldest applicable inventory purchase)

D. The last in, first out (LIFO) method

This method is the opposite of FIFO. Here the newest or last items added to the stock are assumed to be the first ones to be sold. This method is not commonly used. In fact, the IFRS (International Financial Reporting Standards) prohibits LIFO although the United States allows this method.

There are a few reasons a company may use LIFO. Many car dealerships use LIFO 1) because they sell mostly new cars and 2) due to increasing inventory prices, they’re often benefited by selling the most recent items first. Other companies choose LIFO to understate their earnings to show a lower taxable income. Unfortunately, this sometimes leads to unethical activities, which is why the IFRS prohibits it.

Formulas:

- COGS = Units sold x Price per unit from most recent inventory purchase

- Closing inventory = [(units purchased from most recent inventory purchase – units sold) x price per unit from most recent inventory purchase] + [units purchased from oldest applicable inventory purchase x price per unit from oldest applicable inventory purchase]

E. The weighted-average cost method

Like FIFO and LIFO it assumes that prices change over time. Instead of focusing on the first or last products though, it focuses on the average inventory price. It looks at the inventory cost as an average.

Formulas:

- COGS = Units sold x Average price per unit of inventory

- Closing inventory = [(Cost of original units + purchased units costs) – COGS]/average price per unit of inventory

2. Physical inventory counts

This involves counting every item you have in stock to gain an accurate idea of your inventory status. It is recommended to be implemented at least annually and possibly when stock-keeping units (SKU) levels are low. However, this method is very time-consuming.

3. Cycle counting

Since physical inventory counts are a once-in-a-year affair, cycle counting can help manage your inventory. In this approach you count a small amount of inventory on a more frequent basis.

4. Regular reconciliation

This approach keeps you aware of your stock status and helps to identify shrinkage before it gets out of control. It involves comparing the inventory levels in your POS system with the inventory that you physically have in stock. This helps you

- Gauge if there is a mismatch or discrepancy between the two

- Possibly identify the cause

- Avoid it in future

5. Spot checking

In this approach, you count the same portion of your inventory for several weeks in a row to hopefully see patterns and trends. It also indicates potential shrinkage especially in case of high-risk items.

6. ABC analysis

ABC is the abbreviation for “activity-based costing.” The idea behind this approach is that 80% of your revenue comes from the top 20% of your products. Many manufacturing businesses adapt ABC. They categorize their inventory into three categories based on level of importance

- A: High dollar value and low quantity of items

- B: Medium dollar value and medium quantity of items

- C: Low dollar value and high quantity of items

ABC method is time-efficient in that most of your attention is spent on monitoring level A items. After all, they’re the most expensive and most important. This method aids in efficient inventory counting along with monitoring the inventory status of top-performing products.

Tips for an optimized POS inventory management system setup

Running a business comes with its own set of unique challenges. That’s why you need to invest in inventory management systems that help reduce complications. An effective point of sale (POS) inventory system is one such investment. We have put together a few tips that will help you get the best out of your POS inventory system. Take a look:

1. Create a ranking order for categories

These rankings shouldn’t have too many changes over time for you to get consistent data. It is suggested to not have more than ten sub-categories under a top-tier category. This will help you observe and compare sales trends.

2. Inventory counting is essential

We can’t emphasize enough how important counting is when it comes to your inventory. Full counts as well as cycle counts will help you gain an accurate picture of your inventory levels along with identifying shrinkage.

3. All inventory needs to have reorder points

This will ensure that you never run out of a certain product. Your POS can store reorder points for your products, which means you won’t have to monitor the inventory levels of every single product.

Final thoughts

A crucial element of running a business is making sure your inventory is where it should be in accordance with demand. This helps minimize losses. Having an inventory management system takes the guesswork out of the equation as you can always look up your inventory levels. Of course, some things such as shifts in consumer behavior can’t always be predicted.

Having an effective inventory management system will keep you informed and does away with the element of surprise. Being able to optimize your inventory will help you serve your customers better.

Acumen Connections provides credit card processing in Wichita and around the US. However, we offer more than just payment solutions for your business. Our team is dedicated to providing relevant information and business tips to small businesses everywhere. Read more articles here.

Anna Reeve, MBA

Hello! I am Anna with Acumen Connections and I love assisting small businesses in any way I can. I have worked in marketing for businesses of different sizes and industries. I believe that creativity and imagination are the hallmarks of content building. I enjoy creating blogs, social media posts, marketing emails, press releases, website copy, responding to reviews etc.